British consumer behaviour took a dramatic turn in March 2026, as the onset of conflict in the Middle East sparked a significant “dash for fuel” across the United Kingdom.

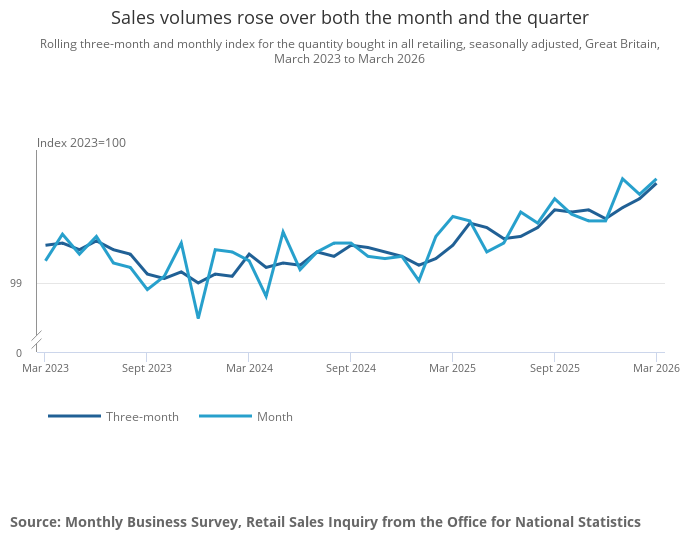

According to the latest data from the Office for National Statistics (ONS) released on Friday, 24 April, retail sales volumes rose by 0.7% in March, comfortably outstripping the 0.1% growth forecast by City economists.

The surge was almost entirely underpinned by a 6.1% leap in automotive fuel sales, the largest monthly increase since 2016 (excluding the volatile pandemic era).

As the Iran war commenced on 28 February, UK motorists rushed to forecourts across the country, fearing supply disruptions and spiralling prices at the pump.

While the headline figure suggests resilience, a deeper analysis reveals a fractured retail landscape, particularly as UK inflation hits 3.3% following the initial energy shock.

Why did UK retail sales unexpectedly jump in March?

The primary driver of the March retail data was a reactive surge in energy consumption. The ONS confirmed that the first few days of March saw “much stronger sales than usual” as news of the conflict broke.

This panic-buying phase contributed to a 12% rise in fuel sales by value, even as the volume of fuel purchased rose by a more modest 6.1%.

Beyond the forecourts, the retail sector saw mixed fortunes:

- Clothing Sales: Rose by 1.2%, aided by a transition from a damp February to unseasonably sunny spells in mid-March.

- Food Sales: Fell by 0.8%, the sharpest decline since August of last year, suggesting that the rising cost of essentials is beginning to force trade-offs in household budgets.

- Non-Fuel Volumes: When stripping out the fuel spike, retail volumes grew by only 0.2%.

The data highlights a “pre-emptive” spending pattern. Consumers prioritised filling their tanks and updating spring wardrobes before the full inflationary impact of the war filtered through to the high street.

How did the Middle East conflict impact specific UK regions?

The “fuel dash” was felt most acutely at motorway service stations and suburban supermarkets with large forecourts. Major transport hubs and arterial routes, including the M1, M6, and M25 corridors, reported significant queues in the first week of March.

- Regional Centres: Areas heavily reliant on car commuting, such as the West Midlands, South Yorkshire, and Greater Manchester, saw the most concentrated spikes in fuel volume sales.

- London and the South East: High-street footfall remained stable due to tourism, but clothing retailers in major hubs like Oxford Street and Westfield Stratford noted a shift toward practical seasonal wear.

- Supermarket Forecourts: Retailers like Tesco and Sainsbury’s reported that while grocery aisles were quieter, their petrol stations were operating at maximum capacity during the initial “dash.”

What are the experts and officials saying about the March surge?

The Office for National Statistics (ONS): “Fuel sales leapt by 6.1% from February… excluding the COVID-19 pandemic period, it was the biggest monthly increase in fuel sales since January 2016.”

Retail sales were 1.6% up in January to March 2026 on the previous three months.

Non-food stores rose by 2.0%, with art selling well and a strong quarter for beauty product stores as retailers reported launching new collections.

Read more ➡️ https://t.co/ggju3L4gqX pic.twitter.com/Pj2L64wTj8

— Office for National Statistics (ONS) (@ONS) April 24, 2026

Thomas Pugh, Chief UK Economist at RSM: “The longer the crisis goes on, the more likely consumers are to adjust their spending habits as confidence wanes. That sets a much tougher outlook for retailers than we were considering before the war.”

GfK Consumer Sentiment Index: The latest GfK report, published Thursday, shows consumer confidence has fallen to its lowest level since October 2023.

The -25 headline score reflects the largest month-on-month drop in a year, indicating that the March spending “bounce” may be a final flourish before a period of retrenchment.

Retail Leaders:

- Sainsbury’s: Stated that the outlook is “clouded” by geopolitical uncertainty, forecasting underlying profits between £975 million and £1.075 billion for the coming year.

- Primark (ABF): Noted that while March was encouraging, trading in April has so far been soft, directly citing the Middle East conflict as a cooling factor for consumer appetite.

How is the “Fuel Dash” affecting the average UK household?

The immediate impact of the 0.7% retail surge is a double-edged sword for the British public.

-

Squeezed Discretionary Income: While growth looks positive on paper, it represents a shift in “wallet share.” Money that might have been spent on leisure or high-end groceries is being diverted to fuel tanks.

-

Transport Costs: Petrol prices rose by approximately 14p per litre (10%) between late February and late March, while diesel saw a steeper 29p (20%) hike.

-

The “Sunshine Effect”: The brief boost in clothing sales suggests that UK shoppers are still responsive to weather patterns, but this “feel-good” spending is being rapidly eclipsed by energy bill fears.

Is the UK heading for a “Technical Recession” in 2026?

As we move into mid-2026, the retail sector faces three significant headwinds that could stall the economy:

-

Monetary Policy Pressure: The Bank of England’s Monetary Policy Committee (MPC) meets on 30 April. With inflation hitting 3.3% in March, there is intense pressure to decide whether to hold rates to support growth or raise them to combat war-driven inflation.

-

Food Security Concerns: The National Farmers’ Union (NFU) has warned that food prices are likely to rise by up to 10% by December 2026 due to higher energy and fertiliser costs linked to the conflict.

-

Fiscal Response: Pressure is mounting on HM Treasury and the Chancellor to consider a temporary reduction in fuel duty, which currently sits at a fixed level, to prevent a total collapse in consumer spending.