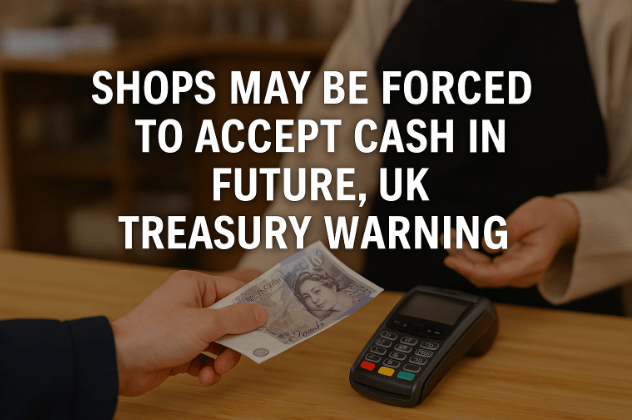

Shops and service providers across the UK could soon be compelled to accept cash, as MPs raise alarms over the potential exclusion of vulnerable communities in an increasingly digital economy.

A recent Treasury Committee report has urged the government to step up efforts to monitor and safeguard cash acceptance. While it stops short of demanding immediate legislative change, the message is clear: action may soon be necessary.

“There may come a time in the future where it becomes necessary for HM Treasury to mandate cash acceptance if appropriate safeguards have not been implemented for those who need physical cash,” the report states.

Unlike countries such as Australia or parts of the EU, where rules to protect cash use are being actively pursued, the UK currently has no laws requiring shops or services to accept cash. Businesses are free to choose their preferred method of payment. Many are opting for card-only systems.

That shift is having real consequences. The committee warns of a growing “poverty premium”—where people who rely on cash face higher prices or fewer options.

Vulnerable groups like the elderly, those with learning difficulties, or individuals fleeing domestic abuse may be hit hardest.

“A sizeable minority depend on being able to use cash,” said Dame Meg Hillier, Chair of the Treasury Committee. She labelled the report a “wake-up call” for policymakers.

MPs didn’t hold back when addressing the government’s lack of oversight. They criticised Whitehall’s inability to track where and how cash is still accepted.

“The government is in the dark on how widely cash is being accepted and that is completely unsustainable,” Dame Meg added. Without urgent improvements, the report warns that people could be shut out of basic services—from leisure centres and theatres to public transport and parking.

There were also serious concerns raised about victims of economic or domestic abuse, who often rely on cash to avoid leaving digital footprints or to regain financial independence.

At the grassroots level, the story of cash is mixed. In Epsom, Surrey, traders at the historic market are adapting. Chris Ilsley, who runs CI Plants, remembers when every transaction was in coins and notes.

Today? Around 70% to 80% of his sales are done by card. “We’ll take anything,” he said. “I prefer the older generation to use card and put their purse away [for safety].”

Tom Cresswell, who owns The Fruit Machine stall nearby, sees a similar trend. “The youngsters don’t ever pay by cash; they pay with their phones and their watches,” he said. “The older gentlemen tend to use cash. Whatever is easier for the customer.”

Post Office Deal Offers Lifeline

There’s been one bit of good news. The Post Office recently announced an extended deal with UK banks, enabling access to basic banking services at local counters until at least 2030. That includes cash withdrawals, deposits, and balance checks.

But for many campaigners, this isn’t enough. Ron Delnevo of the Payments Choice Alliance criticised what he called the committee’s “procrastinating approach” and called for legal guarantees now, not later.

Public support for cash remains robust. The Treasury maintains it is committed to financial inclusion, promising 350 banking hubs nationwide. It also welcomed businesses that continue to accept cash, noting new FCA rules to help them deposit takings more easily.

Still, the pressure is mounting. Without stronger protections, many fear the UK’s cash infrastructure could wither, leaving behind those who still depend on it.

The move towards a cashless society may be convenient for many, but it carries unintended consequences for some of the UK’s most vulnerable. With MPs sounding the alarm, the government faces growing calls to act decisively—before cash becomes a relic and millions are left behind.